Lataa esitys

Esittely latautuu. Ole hyvä ja odota

1

EMISSIONS TRADING Minna-Maari Harmaala

2

EmissionsTrading CONTENTS Background and history to emissions trading The economics of international emissions trading The Kyoto Protocol Emission trading in Finland Business effects of emissions trading

3

WHAT IS EMISSIONS TRADING? EmissionsTrading

4

What is emissions trading? Emissions trading is ”A market-based approach used to control pollution by providing economic incentives for achieving reductions in the emissions of pollutants” (Stavins. 2001) Market-based instruments are aimed at encouraging behavior through market signals rather than through explicit directives or regulations regarding the levels of pollution or the allowed methods and means for reducing them Overall goal is to reduce emissions with minimum cost! EmissionsTrading

Market-based instruments are aimed at encouraging behavior through market signals rather than through explicit directives or regulations regarding the levels of pollution or the allowed methods and means for reducing them Overall goal is to reduce emissions with minimum cost. EmissionsTrading.")

5

Emissions trading in a nutshell Some authority sets a limit on the amount of a pollutant that can be emitted (=cap) This limit is allocated/ given/ sold to companies as emissions permits. The total level of permits must equal the cap. The permit allows the company to emit the amount of the pollutant specified in the permit. If the company can not meet its ”quota” it will either have to buy permits from others, or engage in pollution prevention measures. Theoretically those who can reduce emissions most cheaply will do so, achieving pollution reductions at the least societal cost EmissionsTrading

6

Basic principle of emissions trading In year 1 both companies A and B emit 100 tonnes of CO2. The following year, company A emits 110 tonnes and company B 140 t. The emissions are being reduced by emission reduction measures; each has to reach 90 t. For company A the cost of reducing emissions is 10 EUR/t and for company B 40 EUR/t If both reduce to 90t, total emissions are 180t. It will cost A 200 EUR (20t*10e) and B 2,000 EUR (50t*40e). This is not the COST efficient solution! EmissionsTrading Source: Jussi Nykänen 2006

and B 2,000 EUR (50t*40e). This is not the COST efficient solution. EmissionsTrading Source: Jussi Nykänen")

7

Basic principle of emissions trading, con’t The most cost efficient solution is for A to reduce emissions to 40 tonnes with the cost of (70t*10e) 700 EUR. B does not reduce emissions at all but instead pays A 700e- 200e=500e; in effect buys emission reductions. Total emissions stay at 180t but total costs are one third of the previous total costs. EmissionsTrading Source: Jussi Nykänen 2006

8

Market mechanism? Or almost…? Market mechanisms vs. the command and control approach Command and control often viewed as rigid and inefficient providing little incentive for innovation However, the government sets the cap (=regulatory measure); after this; it’s a market mechanism… until A company fails to comply with the cap/ limit and may be hit with another regulatory measure, fine for example Regulatory measures often increase the cost of production; firms will opt for the least-cost way to comply EmissionsTrading

; after this; it’s a market mechanism… until A company fails to comply with the cap/ limit and may be hit with another regulatory measure, fine for example Regulatory measures often increase the cost of production; firms will opt for the least-cost way to comply EmissionsTrading.")

9

History and background Rather surprisingly emissions trading development can be traced back to the US First simulations were made in the late 60’s; institutionalized for the first time in The Clean Air Act (1977) First cap-and-trade system: 1990 Clean Air Act as part of the US Acid Rain Program. ”The paradigm shift” Later shifting from the US clean air to global climate policy, global carbon markets and the carbon industry EmissionsTrading

10

The IPPC The Intergovernmental Panel on Climate Change (created 1998 under UNEP) Purpose to give “the world a clear scientific view on the current state of climate change and its potential environmental and socio- economic consequences” Massive debate on global climate change; more uncertainties than truths! Policy recommendations included Energy pricing strategies through taxes and subsidies Phasing out existing distortionary policies (certain subsidies & regulation, non-internalisation of externalities) Tradable emission permits Energy efficiency standards Market pull and demonstration programs Etc. EmissionsTrading

Tradable emission permits Energy efficiency standards Market pull and demonstration programs Etc. EmissionsTrading.")

11

An externality? What? Economics dictionary ” An externality is an effect of a purchase or use decision by one set of parties on others who did not have a choice and whose interests were not taken into account. Classic example of a negative externality: pollution, generated by some productive enterprise, and affecting others who had no choice and were probably not taken into account. ” In a competitive market, prices do not reflect the full costs or benefits of producing or consuming a product or service, and too much or too little of the good will be produced or consumed in terms of overall costs and benefits to society. For example, manufacturing that causes pollution imposes costs on the whole society, the good will be overproduced by a competitive market, as the producer does not take into account the external costs when producing the good. The tragedy of the commons (Hardin 1968) EmissionsTrading

EmissionsTrading.")

12

THE ECONOMICS OF EMISSIONS TRADING EmissionsTrading

13

The economics of emissions trading Different countries have a differently sloping Marginal Abatement Cost Curve (MAC) the cost of eliminating an additional unit of pollution For example, countries which have already invested heavily in pollution prevention will have a much higher price tag on further emissions reductions than countries which have invested less International/ global emissions trading was created precisely to exploit these differences air emissions especially know no boundaries! EmissionsTrading

14

MACs and international emissions trading; example EmissionsTrading Total amount of required reductions Market price of emission allowance Efficient allocation (as a result of trade)

")

15

MACs in an individual business Any individual company can and should calculate its own MAC. Simplified: Net Present Value of investment/ saved CO2 emissions Example: A cookie manufacturer is considering an upgrade of its factory lighting. The project will involve changing existing lamps, installation of time-delay switches, occupancy sensors, etc. For an investment of 17,000 EUR to buy and install the new lighting system, the cookie manufacturer will save 2,000 EUR per annum in electricity. The project will save 400 tonnes of CO2 across an investment time frame of four years. Calculate the NPV and MAC. EmissionsTrading

16

Cookie example continued NPV = 17,000 (investment) – 2,000 * 4 (total savings) = 9,000 EUR MAC = 9,000 EUR/400 t CO2 =22,50 EUR/tonne CO2 EmissionsTrading Source: EPA Victoria

– 2,000 * 4 (total savings) = 9,000 EUR MAC = 9,000 EUR/400 t CO2 =22,50 EUR/tonne CO2 EmissionsTrading Source: EPA Victoria")

17

Another cookie example The same cookie manufacturer identifies that some of its equipment can be shut down completely during the weekend. This will have no cost to the business and will save 6,000 EUR and 300 tonnes of CO2 over four years. NPV = 0 – 6,000 EUR = -6,000 EUR MAC = -6,000 EUR/ 300 t CO2 = -20,00 EUR/t CO2 EmissionsTrading Source: EPA Victoria

18

THE KYOTO PROTOCOL EmissionsTrading

19

The Kyoto Protocol An international treaty drafted in 1997 and came into force 2005. The US and Australia are the only industrialised countries in Annex 1 that have not ratified the treaty not bound by its obligations. Intention to reduce emissions from 1990 levels by 2012. Introduces three mechanisms: (1) emissions trading (2) joint implementation JI and (3) clean development mechanisms CDM. These aim to reduce costs and promote technology transfer to developing and underdeveloped countries. EmissionsTrading

emissions trading (2) joint implementation JI and (3) clean development mechanisms CDM. These aim to reduce costs and promote technology transfer to developing and underdeveloped countries. EmissionsTrading.")

20

Annex I There are 40 Annex I countries and the European Union is also a member. Australia, Austria, Belarus, Belgium, Bulgaria, Canada, Croatia, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Japan, Latvia, Liechtenstein, Lithuania, Luxembourg, Monaco, Netherlands, New Zealand, Norway, Poland, Portugal, Romania, Russian Federation, Slovakia, Slovenia, Spain, Sweden, Switzerland, Turkey, Ukraine, United Kingdom, United States of America EmissionsTrading

21

Joint Implementation Allows a country with an emission reduction or limitation commitment under the Kyoto Protocol to earn emission reduction units (ERUs) from an emission-reduction or emission removal project in another Annex B Party, which can be counted towards meeting its Kyoto target. Joint implementation offers Parties a flexible and cost-efficient means of fulfilling a part of their Kyoto commitments, while the host Party benefits from foreign investment and technology transfer. A JI project must provide a reduction in emissions by sources, or an enhancement of removals by sinks, that is additional to what would otherwise have occurred. EmissionsTrading

22

…JI Most JI’s in former Soviet states and transition economies in central and eastern Europe. Currently most projects in Russia and Ukraine. CO2 reductions are generally cheaper in these countries. The total emissions or emission allowances stay unchanged with a JI. JI takes place between two countries, which each have an emissions reduction target! Examples are windpower, and combined heat and power production. EmissionsTrading

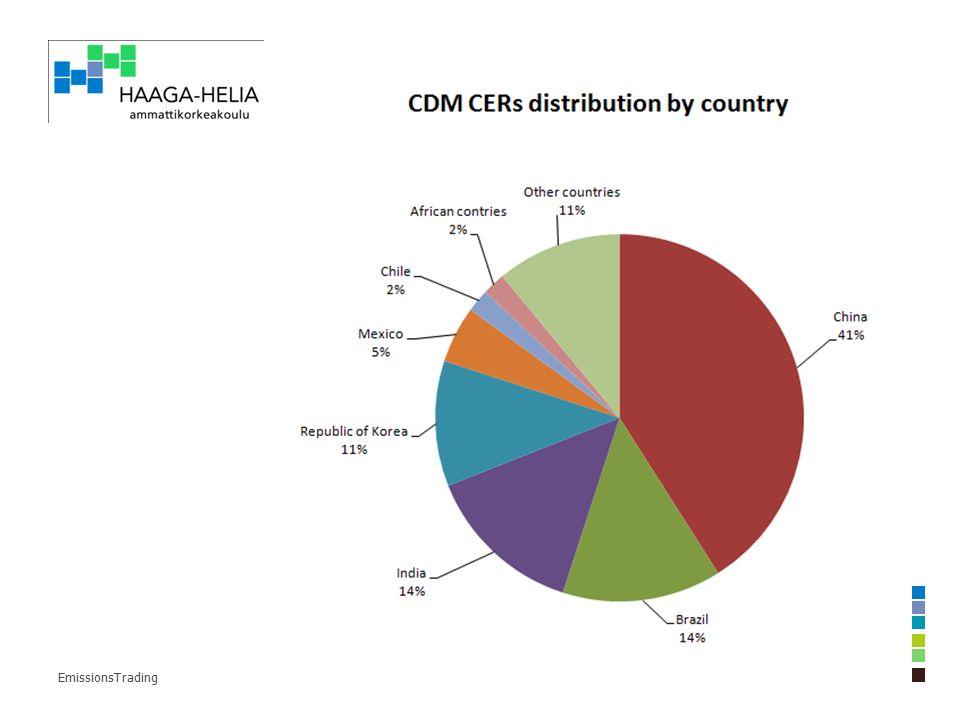

23

Clean Development Mechanism, CDM Allows a country with an emission-reduction or emission-limitation commitment under the Kyoto Protocol to implement an emission- reduction project in developing countries. Such projects can earn saleable certified emission reduction (CER) credits, which can be counted towards meeting Kyoto targets. The mechanism is seen by many as a trailblazer. It is the first global, environmental investment and credit scheme of its kind, providing a standardized emissions offset instrument, CERs. For example a rural electrification project using solar panels or the installation of more energy-efficient boilers. The mechanism stimulates sustainable development and emission reductions, while giving industrialized countries some flexibility in how they meet their emission reduction or limitation targets. EmissionsTrading

credits, which can be counted towards meeting Kyoto targets. The mechanism is seen by many as a trailblazer. It is the first global, environmental investment and credit scheme of its kind, providing a standardized emissions offset instrument, CERs. For example a rural electrification project using solar panels or the installation of more energy-efficient boilers. The mechanism stimulates sustainable development and emission reductions, while giving industrialized countries some flexibility in how they meet their emission reduction or limitation targets. EmissionsTrading.")

25

EMISSIONS TRADING IN FINLAND EmissionsTrading

26

Emissions trading in Finland Finland has adopted laws and regulations concerning emissions trading. Energy market authority (Energiamarkkinavirasto) is the national emissions trading authority. EMV is responsible for issuing and monitoring emission permits, maintaining the emissions trading register, monitoring the emissions trading scheme and adherence to regulation and accepting emission trading auditors. The Emissions Trading Act is applied to carbon dioxide emissions of combustion installations with a rated thermal input of more than 20 MW and of the smaller combustion installations connected to the same district heating network, of mineral oil refineries and coke ovens, as well as of certain installations and processes of the steel, mineral and forest industries. EmissionsTrading

is the national emissions trading authority. EMV is responsible for issuing and monitoring emission permits, maintaining the emissions trading register, monitoring the emissions trading scheme and adherence to regulation and accepting emission trading auditors. The Emissions Trading Act is applied to carbon dioxide emissions of combustion installations with a rated thermal input of more than 20 MW and of the smaller combustion installations connected to the same district heating network, of mineral oil refineries and coke ovens, as well as of certain installations and processes of the steel, mineral and forest industries. EmissionsTrading.")

27

Emissions trading in Finland 2009 In Finland, the number of installations needing a permit is around 530. Combined emissions in 2009 from Finnish installations were 34,4 million tonnes CO2. Emission permits allocated free of charge were enough to cover this and in fact permits for 2,7 million tonnes CO2 were left over. The global recession decreased the need for emissions permits a little, except in the energy industry which needed permits for 1,8 million tonnes CO2 more than it was originally allocated EmissionsTrading

28

What does an emission permit cost? Cost of en emission permit (EUADEC-10) 15.9.2009 – 14.9.2010 (EUR/t CO2) EmissionsTrading

– (EUR/t CO2) EmissionsTrading.")

29

EFFECTS OF EMISSION TRADING ON BUSINESS EmissionsTrading

30

Emissions trading in practice Emissions trading brings some additional issues to the business agenda: Emissions permit; must be applied for much in the same way as an environmental permit Emissions registry; company must open an account in the national emissions registry Emissions monitoring and returning emission allowances; company must monitor and verify emissions and return the required emission allowances to EMV Evaluate emission reduction possibilities Emissions trading and trading strategy Emissions trading in accounting… EmissionsTrading

31

Emissions trading in accounting Emissions trading sets certain requirements for the accounting department! IFRIC (International Financial Reporting Interpretations Committee) withdrew an interpretation on this issue in 2005 due to conflicts in measurement and reporting. It is now being worked on again and ”in the initial stages of completion” In Finland there are interpretation for accounting and taxation purposes Emission allowances are to be treated as intangible rights in the company’s fixed assets (aineettomia oikeuksia käyttöomaisuudessa) EmissionsTrading

withdrew an interpretation on this issue in 2005 due to conflicts in measurement and reporting. It is now being worked on again and in the initial stages of completion In Finland there are interpretation for accounting and taxation purposes Emission allowances are to be treated as intangible rights in the company’s fixed assets (aineettomia oikeuksia käyttöomaisuudessa) EmissionsTrading.")

32

KILAn lausunto 1767 (15.11.2005) Hyvän kirjanpitotavan mukaista on perustaa päästöoikeuksien kirjanpitokäsittely ns. nettomenettelyyn. Jos toteutuneet päästötonnit ylittävät saadut oikeudet, tehdään ylimeneviä tonneja vastaava kulukirjaus tilinpäätöshetken markkinahinnalla ja pakolliset varaukset vastatilinä. Kuitenkin siinä tapauksessa, että puuttuvien päästöoikeuksien hankinta on sidottu sopimuksella tai muuten tietyn hintaiseksi, kulukirjaus tehdään lähtökohtaisesti sen mukaisena. Jos taas toteutuneet tonnit alittavat saadut oikeudet, kirjanpitovelvollisella on taseen ulkopuolista varallisuutta, joka tulee ilmoittaa liitetietoina. Toisaalta päästöoikeuksien ostot ja myynnit kirjataan liiketapahtumina suoriteperusteisesti. Jotta nettomenettely antaisi oikean ja riittävän kuvan päästöoikeuksien vaikutuksista, kirjanpitovelvollisen tulee lisäksi tilinpäätöksen liitetietona kuvata päästöoikeuksiensa, toteutuneiden päästöjen ja käymänsä päästökaupan kokonais- ja hintatilanne sekä vaikutus tulokseen ja taloudelliseen asemaan. Vastaavalla tavalla menetellään myös osavuosikatsauksen tai muun välitilinpäätöksen laadinnassa ottaen kuitenkin koko tilikauden arvioidut päästöt huomioon olennaisuuden periaatteen mukaisesti. EmissionsTrading

33

Some Finnish examples Ruukki annual report EmissionsTrading

34

Ruukilla ei mainintaa päästökaupasta varauksissa EmissionsTrading

35

Ruukki annual report

36

UPM annual report EmissionsTrading

37

UPM EmissionsTrading

38

UPM

39

EmissionsTrading UPM annual report

40

Päästöoikeudet Suomen verotuksessa Maksutta jaettujen päästöoikeuksien hankintameno on 0 euroa. Arvonlisäverotuksessa päästöoikeuden myynti on palvelun myyntiä, johon sovelletaan arvonlisäverolain 68 §:n immateriaalipalveluja koskevia säännöksiä. Elinkeinonharjoittajille myydyt immateriaalipalvelut verotetaan Suomessa, jos ne luovutetaan ostajan täällä olevaan kiinteään toimipaikkaan. Päästöoikeus ei ole varainsiirtoverolain mukainen arvopaperi, jonka omistusoikeuden luovutuksesta luovutuksensaajan olisi maksettava varainsiirtoveroa. Päästöoikeuden ylitysmaksu on luonteeltaan elinkeinotulon verottamisesta annetun lain 16 §:n 5 kohdan mukainen sanktioluonteinen maksuseuraamus, joten päästöoikeuden ylitysmaksu ei ole tulon hankkimisesta tai säilyttämisestä johtunut vähennyskelpoinen meno. Päästöoikeuden ylitysmaksua käsitellään verotuksessa siten vähennyskelvottomana eränä EmissionsTrading

Samankaltaiset esitykset